With inflation skyrocketing and interest rates on the rise, advisers are telling us debt is becoming more of a talking point in client meetings.

It’s probably little surprise. Debt is already such a perennial concern for Australians. Earlier this year, when Adviser Ratings asked more than 2000 consumers how they’d spend a spare $10,000 if they had it, the most popular answer was to pay down debt. Meanwhile, hundreds said they’d like to learn more about managing debt.

As inflation continues, some economists – including Deutsche Bank’s Phil O’Donoghue – are tipping the next Reserve Bank rate hike to be as high as 0.75 percentage points, which means things could get worse quickly for those already worried about mortgage debt.

As a result, advisers may find themselves fielding more questions from concerned clients about restructuring mortgages, budgeting, making tax adjustments and using additional home loan features.

Of course, clients and consumers aren’t the only ones the current economic conditions affect. We thought it would be worth looking at how practices themselves are faring when it comes to debt and overall balance sheets.

The impact of rising rates on advice businesses

For many advisers, the march north in the cash rate may be the first they’ve ever experienced first-hand. With cash forecasts expected to hit 3.5 per cent next year, the burden of interest rate increases is likely to be shared by indebted small businesses (advice firms), not just mortgage holders.

With practice owners drawing down anywhere between $140,000 and $160,000 from their practice, those with company debt – which averages $350,000 - could see a real wage impact up to $10,000 per annum. This is on top of normal inflationary pressures. Practice efficiencies will become more important as a key focus for many advisers for the year ahead.

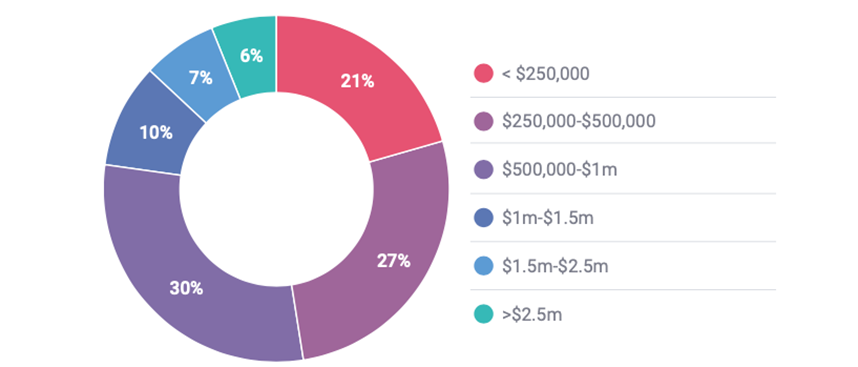

Figure 1 – Practice revenue

Source: Adviser Ratings

Where practices stand

Research conducted for our most recent Landscape Report delivers further insights about the health of advice businesses.

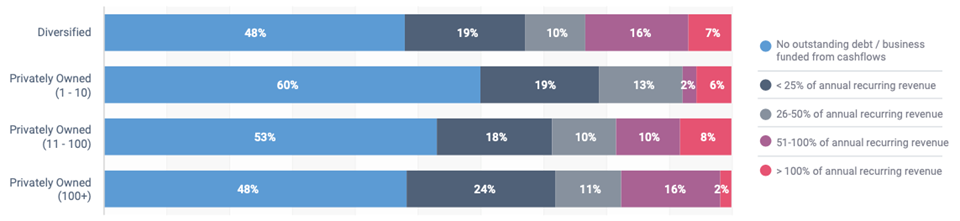

Overall, we found the majority of practices had no outstanding debt or were funding their business through cashflow.

Figure 2 – Practice debt

Source: Adviser Ratings

Practices at the smaller end of the scale (1-10 advisers) generally carried lower levels of debt, while diversified and large practices displayed more aggressive debt-backed growth strategies. Almost one-in-five businesses with more than 11 advisers had practice debt exceeding half of their annual recurring revenue, compared with less than one-in-10 boutiques.

A small proportion of businesses of all sizes had a debt ratio more than 100 per cent of their recurring revenue during our survey period. Among large businesses, 2 per cent fell into this category, compared with 6 per cent of boutiques. For the latter, this could mean sustainability challenges, especially in the face of rising rates.

Access to funding

Our analysis found the low levels of debt also reflected a hesitation among some businesses to use debt-funded investment to grow. Also, businesses that seek debt funding aren’t necessarily getting it. Banks have been heavily scrutinising practices’ growth strategies and some have been unable to obtain funding once their business plans have been placed under the microscope.

While lower debt levels may be good news during a time of successive rate hikes, profitability concerns continue to pervade advice businesses, especially small or low-revenue firms. One-in-five practices reported revenue below $250,000 and most of those had no profit.

Article by:

Comments0