The relationship between advisers and insurers has certainly been put to the test in the past few years, with both parties wading through a raft of reforms, pricing changes and structural challenges.

Amid this, advisers’ sentiment towards insurers has been largely negative. As advisers continue to tackle professional standards and low commissions, recent changes to the pricing of individual disability income insurance (IDII) has further soured feelings towards the insurance market.

Incumbents vs. challengers

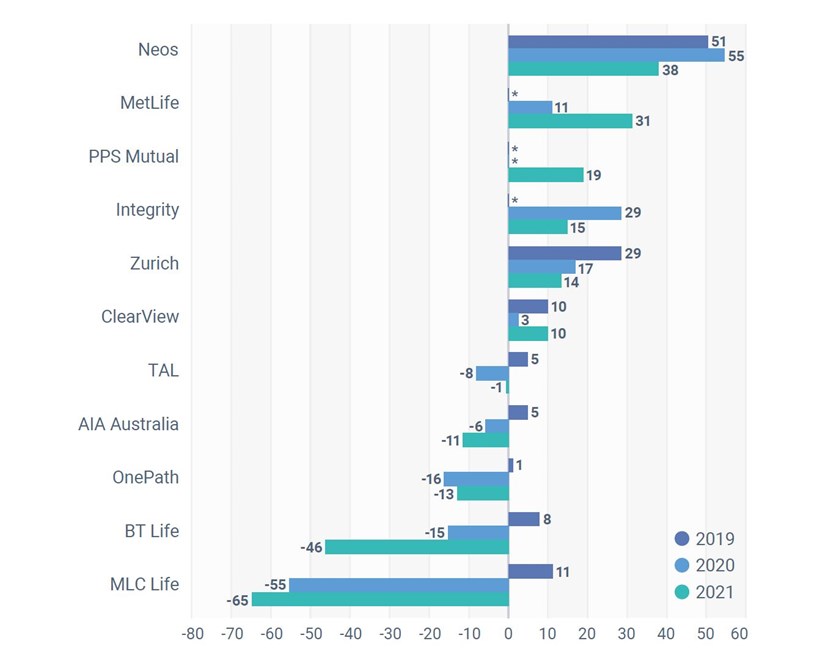

Not all insurers are viewed equally. We’ve continued to see warmer sentiment towards the market challengers, who are offering greater adviser support and aren’t encumbered by the same legacy issues as incumbents. As Figure 1 shows, Neos in particular has reflected this trend in the past few years.

Of course, there are also exceptions to the incumbent generalisation, with both Zurich and ClearView still in positive NPS territory. In 2021, MetLife similarly won favour among the adviser community for its IDII pricing moves.

At the other end of the spectrum, MLC Life has seen its fortunes sour in two short years. One adviser said it has “too many bugs to recommend” post-upgrade, with sub-optimal adviser support.

Figure 1 – Net promoter score (NPS) by insurer, 2019-21

Source: Adviser Ratings' 2022 Australian Financial Advice Landscape Report. Note: * indicates insufficient data.

Support makes the difference

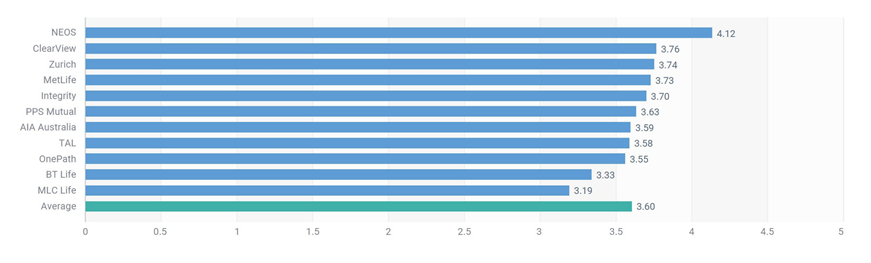

It’s probably little surprise that adviser support is one of the most prized insurance offerings, along with the ability to form a decision quickly. In the absence of a well-integrated technology system, advisers expect a well-trained team of support staff that can guide them through the process.

Most insurers are recognising the need to meet this benchmark, with newer player Neos and incumbent Zurich leading the field (see Figure 2).

One adviser in a two-person practice commented: “I really hope Neos Life can continue their service and delivery of product to market (as some insurers struggle with after initially dominating when they first enter the market, eventually becoming ‘bogged down’). They’ve been nothing but a pleasure to deal with on every front.”

On Zurich, an adviser from a solo practice said: “Overall, a very good company to deal with. They offer me a one-person contact point to handle all the admin issues and a dedicated underwriter.”

Figure 2: How advisers rank insurers on adviser support

Source: Adviser Ratings' 2022 Australian Financial Advice Landscape Report. Note: n = 2,954 reviews, Bayesian statistical analysis used.

Given insurers will increasingly have to pivot away from serving advisers who are risk-only or mostly risk, towards advisers who write a lower volume of risk, their future service offering will be critical. Will they rise to the occasion?

Article by:

Comments2

"Jeremy is spot on but I would make a few detailed additional comments. In amongst all the noise from APRA about the recent changes to IP contracts, there was a "demand" that the insurers develop a much larger capacity to gather data on claims and interpret that data. Seems APRA had discovered, like it does with most things in life insurance eventually, that there was no real usable data being collected by insurers on income protection claims. Quell surprise! The majority of well-established insurers struggle with demands from advisers in a technological age. There are at least two insurers that I can think of who still send out by SNAIL MAIL adviser copies of annual renewals. Advisers have to scan those renewals to add them to the compulsory CRMs. That's inefficient. Most CRMs have the function to flick an email straight off onto the client's file. But wait there's more: those renewal notices usually have about two pages of actual print, spread over four pages. No consideration of the environment in that exercise. Certificates of Currency or equivalents which must be sourced before providing replacement advice. The most recent certificates I have sighted do not list medical loadings and exclusions. To do that the adviser has to spend hours on the phone with a poorly trained call-centre operator. For those with more modern CRMs, downloads of policy data are theoretically available direct from insurers. But only some insurers currently make that information available easily. And there's many an experienced adviser who can tell tall tales about how a policy "download" from their favorite insurer resulted in the CRM having to be started again from scratch. I can hear the insurers whingeing from where I sit. Obviously there will be costs involved in improving the service by insurers to advisers. And none of us want to see increased premiums, so as Treasurers around the world are saying, something has to give. I suggest that the CEOs and their lovely fat bonuses should be first cab off the rank, particularly those who are apparently on retention bonuses and have never talked to advisers as to as to what their retention activity should look like."

Bill Brown 09:43 on 23 Jun 22

"The wish list from Advisers has not changed. It has always been about being able to time and cost effectively work with the Insurers to bring about the best outcome for clients. What has become a major issue is that the cost, time and risk of providing all the services that Advisers bring to the table has risen exponentially, which must be resolved for the Industry to rebuild. It is a simple problem to fix in the Life Insurance sector. What is needed is for the Government and Regulators to properly address the issues and bring in the right Regulatory framework that incentivizes and protects everyone in the link. Reducing the time, cost and risks to do Business, with increased efficiencies, utilising technology that is an enabler for Advisers to do what they do best, will turn it all around so Australians will be better covered, have more peace of mind and in turn, create the economic benefits to Australia that will run into the multi-Billions of dollars."

Jeremy Wright 16:12 on 22 Jun 22