Financial advisers are calling for swift action on the Quality of Advice Review recommendations, with many backing the view that reforms should be delivered now and tweaked later.

Earlier this month, reviewer Michelle Levy – who delivered the report to the Federal Government in December last year – wrote an open letter for the Financial Review encouraging the adoption of her suggested changes.

“If they need some refinement, it is better that that happens afterwards. If there is some poor conduct (and there is poor conduct now, too), ASIC has all the powers and tools it needs to put a quick stop to it,” she wrote.

Last week, the Minister for Financial Services and Assistant Treasurer Stephen Jones indicated at a post-Budget Financial Services Council webinar that further detail on the next steps would be released in the coming weeks.

Ms Levy made 13 recommendations, including a “good advice” provision, repealing the current best-interests duty in favour of a statutory duty, and simplifying disclosure requirements. The latter has been listed by adviser groups as a “quick win” that could be implemented quickly, along with changes to how advice records are provided.

The recommendations are aimed at improving consumer access and affordability and previous Adviser Ratings research has found broad support for them – particularly the removal of Statement of Advice requirements.

Act now and refine later?

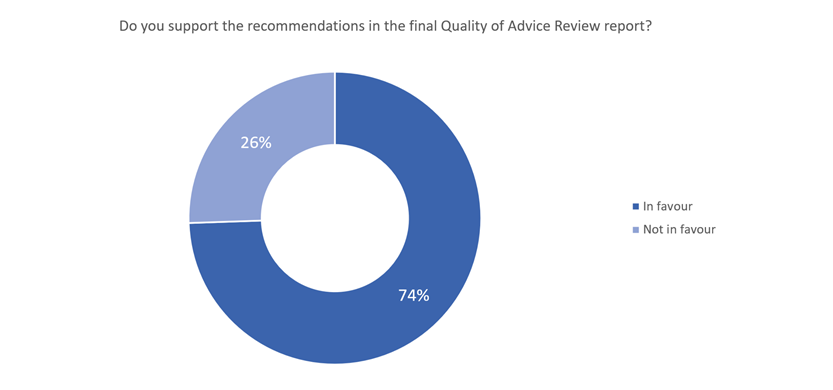

When we asked advisers whether they think the core recommendations should be put in place now and polished later, close to three-in-four were in favour.

Figure 1 – Adviser poll: ‘Do you think the Quality of Advice Review core recommendations should be implemented now and refined later?’

Source: Adviser Ratings

Demand and supply

In her op-ed for the Financial Review, Ms Levy argued many Australians were struggling with mortgage payments, savings and rent, but were largely unable to access the assistance of financial advisers for help make decisions.

Research from our most recent Landscape Report shows many Australians are turning to news media and family or friends for financial information in the absence of a qualified financial adviser, with more than one-in-20 getting their financial information from social media.

Meanwhile, advisers have been trying to meet demand by carrying a higher client load. The average adviser saw 119 clients in 2022, compared with 103 the previous year.

In the past few years, we’ve also seen advisers take on a much higher volume of one-off clients. Between 2020 and 2022, one-off advice jumped 40 per cent for the average adviser. The traffic is coming from a range of avenues, including referrals from colleagues who have left the profession and piecemeal requests from new clients.

The Quality of Advice Review recommended a larger role for super funds and digital advice to help fill the advice gap.

Article by:

Comments3

"Has Michelle Levy or any other individual involved in this shambled waste of time and money, even met a financial adviser? I hope they were paid a lot of money for this because they will need somewhere to hide after people come forward to complain about the poor “advice” provided by their trusted industry fund call centre because their insurance policies don’t pay and their unlisted assets are overvalued. Then it will come out that profit to members means they get whatever is left over after paying expenses, tax, the unions, board directors, Canstar, the Barefoot Investor. They won’t be paying any fees to ASIC. Why do industry funds need regulation when the unions are involved? "

Anonymous 00:21 on 02 Jun 23

"The education standards between non-relevant and relevant should be equal. Otherwise how would a non-relevant provider without any education know what good advice is?"

Autonomous 14:41 on 17 May 23

"without some education requirements for non relevant providers, it's an open door for super funds & big institutions to flout the boundaries of good advice with consumers paying the price. A minimum Advanced Diploma should be required before employed staff deliver any advice."

Michael 14:21 on 17 May 23