Financial advisers often spend countless hours helping their clients make sure their business and succession planning is sorted. When it comes to their own future plans, however, things may look a bit murkier.

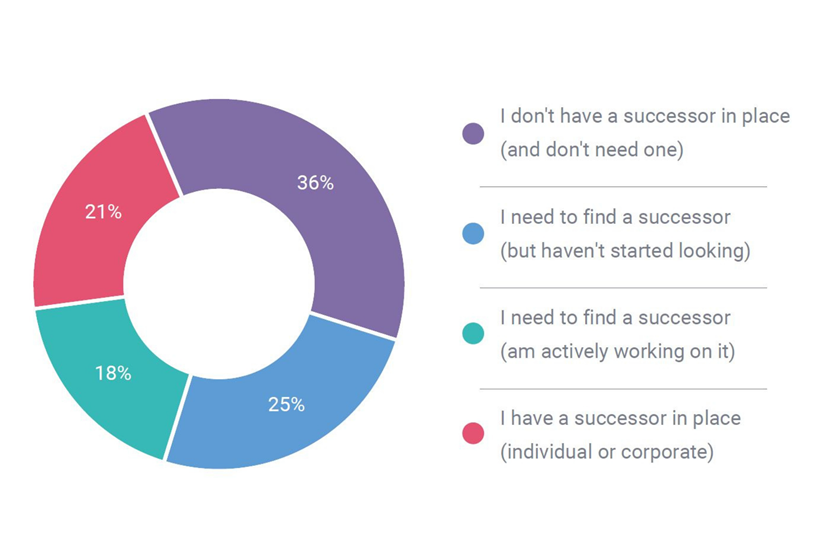

Amid the rapid industry change we’ve seen in the past few years, Adviser Ratings research shows almost 80 per cent of practice owners have not selected a successor for their business. From that cohort, more than half say they’ll need one.

Even so, some businesses are yet to start auditioning potential parties to take the reins. We’re told there are a few things that have complicated the process, including talent supply shortages within the profession and specific requirements that are hard to match. Nonetheless, two-thirds of practice owners recognise succession as a priority to ensure their clients are looked after if something unfortunate happens.

Increasingly, advisers are eyeing mergers and acquisitions – sometimes as a succession strategy – to grow and protect their business. In fact, 23 per cent of advice businesses listed an M&A as a major change they’re looking to make in the future.

Figure 1: Business succession

Source: Adviser Ratings' 2022 Australian Financial Advice Landscape Report

Business plans

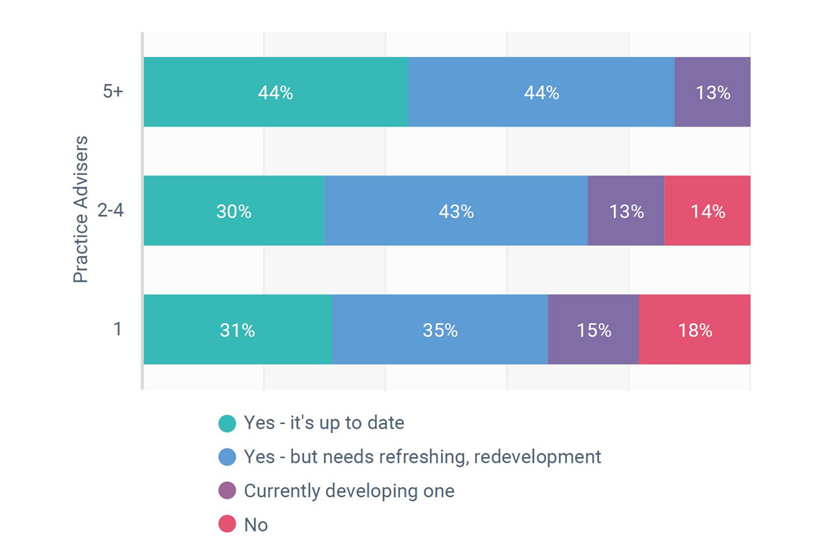

As time-poor advisers grapple with increasing workloads, succession isn’t the only planning area where some businesses say they’ve fallen behind. While most practices recognise having a future roadmap is critical, many admit their business plan needs a refresh. Less than a third of solo and small practices (1-4 advisers) say they’ve got an up-to-date business plan, compared with 44 per cent of mid- to large-size firms (5+ advisers). In fact, a minority of smaller practices have no business plan at all. Fourteen per cent of small firms and 18 per cent of solo operators fall into this category, while a similar proportion across all firm sizes have a plan in development.

Figure 2: Business plans by firm size

Source: Adviser Ratings' 2022 Australian Financial Advice Landscape Report

Having a business plan is often necessary for financing or to attract investors or buyers; however, it can also make sure the practice is on the right track with its goals and prepared for potential hurdles. Some practices use business plans to map out client growth and retention strategies, to prepare for different market scenarios, and to plan communications and marketing activities. These priorities are particularly relevant to growing firms, which need staff to be on the same page about the practice’s direction.

Regardless of the size of the business, having a plan for the future can help size up whether a practice is achieving what it should, especially in a turbulent market like the one we find ourselves in now.

Article by:

Comments0