Four years on from the Hayne Royal Commission, Treasury is revisiting the industry’s professional evolution and whether it has improved the quality, affordability and accessibility of advice.

Our analysis shows advice quality has improved, but we think there is more that can be done to help both advisers and consumers navigate these complex times. As such, here are four recommendations we provided to Treasury’s Quality of Advice Review.

1. Measuring improvements in advice quality

In the past few years, the advice industry has been re-shaped through several legislative changes, but there has not been an industry-wide barometer to measure the success of these actions.

Our analysis indicates reforms have resulted in improvements to the quality of both advisers and licensees and we think both the industry and consumers should have broad access to the information to help them make better decisions.

To further assess the effectiveness of current and future reforms, we believe an independent metric or scoring system should be used to examine the quality of financial advice dispensed, the likelihood of misconduct (based on risk factors) and client satisfaction.

The quality of advice being delivered by active advisers today is better than ever, and we want to ensure the term “financial adviser” is representative of high quality.

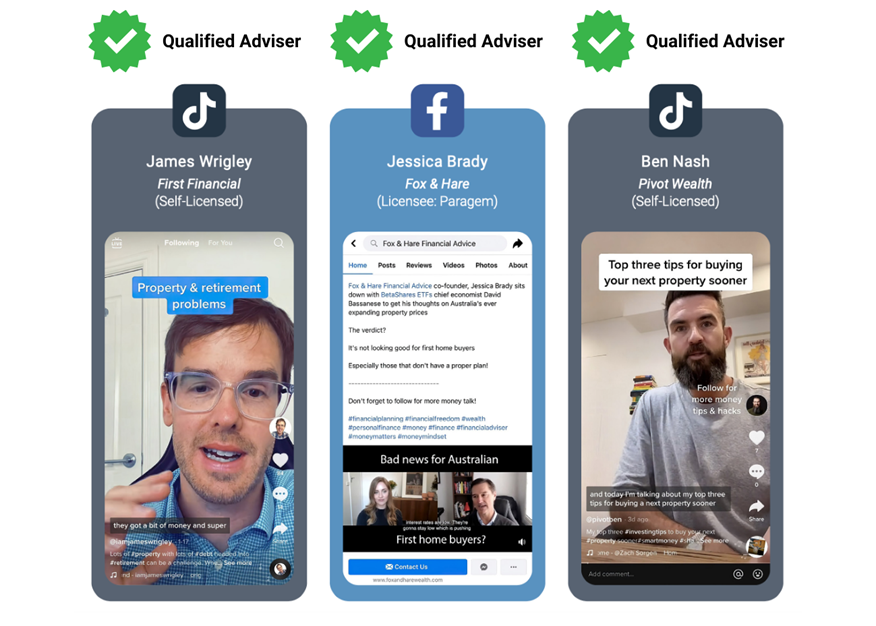

2. Distinguishing advisers from influencers

Financial influencers – or ‘finfluencers’ – have captured the attention of millions of Australians. It is often difficult for viewers to distinguish between qualified financial advisers and those who fall short of the benchmark.

While the Australian Securities and Investments Commission has issued a stern warning to unqualified finfluencers, it is difficult to monitor all of the financial videos on social media.

We think a cost-effective alternative is to present qualified financial advisers with a unique mark or logo to separate them from other content makers.

Figure 1 – Marking qualified advisers on social media

Source: Adviser Ratings

3. Making financial advice tax deductible

Our analysis shows fewer than 2 million Australians are seeing a financial adviser, but a much higher proportion want or need financial advice.

To help with this, we think clients should be able to claim up to $3000 in deductible expenses for seeing an approved financial adviser, given the median advice fee is $3526.

We also recommend two new tax deductions for financial advice: one for costs people incur establishing a financial plan, another for advice that does not relate to assets or investments that presently generate taxable income.

4. Protecting consumers by redefining ‘sophisticated investor’ status

Clients who are defined as ‘sophisticated investors’ are not eligible for the same consumer protections as retail clients, due to their income and assets.

In some cases, this has exposed investors to significant financial risk with limited recourse, because the threshold for what constitutes a sophisticated investor has remained at $250,000 in income and $2.5 million in assets for decades. This is despite property prices rising more than 400 per cent in the same period, CoreLogic data shows.

We believe the threshold is out of date and should be revisited in a more holistic way. This could be achieved by implementing a knowledge test or removing the family home from the assets included when determining sophisticated investor status.

More immediately, we believe the wholesale threshold should be lifted to $300,000 in income for two consecutive years and $5 million in assets. Similarly, advisers should be re-categorised as retail advisers when they manage clients who fall beneath these new limits.

Article by:

Comments2

"I agree with most of what has been written, but also take exception to the last point. There are very few instances of investors being sold "dud" financial products genuinely aimed at wholesale investors. Indeed as a "wholesale only" adviser, I take exception to the current loop-hole whereby any investor able to invest a minimum $500k is able to invest in a "wholesale" product, without satisfying any the other test.. Therefore raising this amount to $5M would immediately reduce these risks without imposing onerous burdens on the majority of genuine wholesale investors & their advisers who continue to do the right thing... "

James Waggett 21:44 on 29 Jun 22

"I agree with most of what has been written, but take exception to the last point. Yes, without doubt, the "sophisticated investor" needs to be changed, and preferably renamed as having $5 million does not make you sophisticated on financial matters. But I do not want to be classed as a "retail adviser". I don't work in a shop; it is demeaning and will confuse clients."

Chris 14:43 on 29 Jun 22