“Will the capital gain from the sale of a property affect my pension? The profit from the sale has paid down the mortgage from my payment protection insurance."

- Question from Lenore in Redland Bay, QLD

Top answer provided by:

David Debono

Hi Lenore,

Congratulations on achieving the great Aussie dream of paying off your mortgage.

The answer to this question will depend on 2 things, the property that you sold and what other income you may be receiving.

Firstly, it is worth mentioning that capital gains or profits from that sale of assets isn’t assessed as income from Centrelink so that alone won’t affect your pension - it just depends where the sale proceeds end up.

If the property that you sold was an investment asset and was previously assessed under the assets test, then your assessable asset value will potentially decrease therefore, potentially increasing your age pension depending on what other assessable other assets you have. However, if you sold your primary residence that was previously asset text exempt, the balance of your sale proceeds after you pay off your mortgage may potentially increase your assessable assets and decrease your pension entitlement.

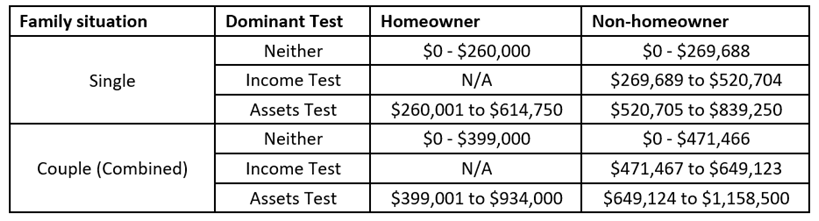

The amount of pension a person is entitled to is based on their assets and income. The rate of payment is calculated under both the income and assets test. The test that results in the lower rate is the one that applies.

The ‘crossover point’ is the point at which a person switches from being affected by the income test to being affected by the assets test. That is, where an additional amount of assets (whether financial investments or not), would lead to a reduction in pension entitlements under the assets test rather than the income test.

The below table shows the levels at which a pension is payable under either test, where the income test is the dominant test and where the assets test is the dominant test. The figures assume that the person(s) hold non-income producing lifestyle assets of $20,000 with all remaining assets being financial investments and subject to deeming. The asset numbers in the table exclude lifestyle assets. For example, a single homeowner who has $20,000 of non-income producing lifestyle assets plus $260,000 of financial investments (i.e. a total of $280,000) will get full pension under both the income and assets test.

Importantly, for a single homeowner and couple homeowner based on the above assumptions (i.e. $20,000 of non-income producing lifestyle assets with all remaining assets being financial investment), the income test is never the dominant test and thus there is no crossover point. That is, a person in this situation will either get full pension or a part pension reduced under the assets test.

It is important to understand what type of asset that you are disposing off and if you are assessed under the assets test of the income test to determine whether or not the capital gain from the sale of your property will affect your pension.

There are calculators available on the Centrelink website which you can use to estimate your entitlement after the sale of your property.

This will give you a clear indication of what your future pension payments will be.

I hope this goes some way to answering your question, but ultimately personalised advice will ensure that you receive the full pension entitlements that you are due.

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0