“I want to ensure that my superannuation is helping me head towards a comfortable retirement. Could you explain the benefits and drawbacks of different types of super funds, and how I can choose the one that's best suited to my retirement goals?"

-Question from Noah in Fremantle, Western Australia

Top answer provided by:

Kieren James

This is a great question Noah, as unfortunately we are not taught properly about superannuation in school and yet it will form one of the greatest retirement assets for most Australians.

First thing to understand is the true power of superannuation, driven by the significant tax benefits and compounding effect over time, even prior to investment earnings. Many people miss this concept and fail to understand why superannuation is so effective.

In choosing a superfund, there is no “one size fits all”. All options are going to have pros and cons and need to be married to the individual’s own circumstances, level of investment, degree of involvement and types of assets to be held etc. The initial criteria to consider should be:

-Functionality – does the fund provide the investment flexibility, account access and reporting you are seeking?

-Capability – is the fund good at administration, including processing times with minimum errors, and customer service?

-Cost – is the fund cost competitive against their peers?

Note: I’m not referring to any investment returns in this response. This is because the investment returns are driven by the investment selections made by the individual, within the particular fund chosen, and not a key driver of choosing the fund (administration) itself.

There are basically three types of super funds (administration) for most of us to consider; Retail funds, Industry funds, and Self-Managed Super Funds (SMSF).

Note: I have not covered Defined Benefit funds, Small APRA funds, or untaxed super funds here, which are less common and out of scope for this response.

Retail funds are products offered by a corporation with shareholders. They allow broad investment opportunities across a large array of internal and external managed funds and direct shares through a “Master Trust” or “Wrap Account”. The latter often appropriate for balances above $500,000 and/or those seeking far greater investment flexibility and taxation control. Retail funds can provide access to hundreds of different investment options from leading fund managers globally.

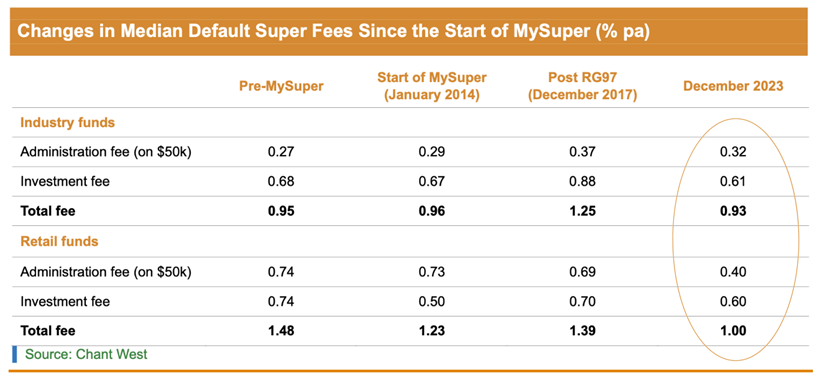

In contrast, Industry funds generally offer a small list of investment options (say 5-10 on average) to choose from. These are generally internally managed and suited to those who want no real involvement in portfolio construction and tax management. Industry funds operate more like a co-operative than a corporation and do not have shareholders, thus the mantra “profits to members” has been their long-running mantra. Industry funds have grown to become some of the largest funds in Australia and have helped restructure superannuation product costs over time. However, the original fee argument no longer holds value, as the fees between Retail and Industry funds has all but vanished (down to just 0.07% pa – see figure 1), with some individual Retail funds at lower costs to Industry funds.

Figure 1 – Changes in Median Default Super Fees Since the Start of MySuper

Source: Chant West

The decision between Retail funds and Industry funds we now find is less about cost, more about the level of investment flexibility and transparency, and what degree of personal tax management on asset sales within the fund the individual is seeking.

Note: you may also be in a Corporate super fund arrangement, which is most often a separately structured group plan that is derived from either a Retail or Industry fund. These may often carry additional benefits only available to you as an employee of that organisation, including discounted or subsidised insurance covers, lower administration fees, or other benefits. It is always important to check what those arrangements might be before deciding to move to another fund.

Self-Managed Superannuation Funds (SMSF) go the next step in allowing greater investment flexibility including direct property or business assets, even valuable artworks and collectibles, which cannot be achieved through Retail or Industry funds. These should be considered specific purpose funds and not taken lightly, as running an SMSF means taking on the trustee responsibilities of that fund. SMSF requires establishment costs and ongoing accounting and auditing costs in addition to any investment management costs and can be more expensive, particularly at lower balances. It is generally accepted that the minimum suggested balance for starting a SMSF is $500,000 or more, although if only investing in direct shares and managed funds, the same results can often be achieved through a Wrap account at a far lower cost. We usually consider SMSF most appropriate for larger account balances seeking specific real estate or business asset investment, as mentioned above.

For most Australians, a quality Retail or Industry fund will be the appropriate choice to make. We also encourage seeking professional advice to ensure you are choosing not only the right fund to suit your needs, but also the most appropriate investment option(s) within that fund.

Kieren James GDipFP MBA CFP®

Priority Advisory Group

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0