“I'm 28 years old and my only debt is my mortgage. I have a few thousand I was looking to invest. I'm seeking investment options that offer both security and high returns."

-Question from Rajesh in Brisbane, QLD

Top answer provided by:

Andrew White

Hi Rajesh, thanks for the question and well done for having purchased a property at the age of 28 – I know that many are struggling to enter the property market so having a foot on the ladder is a great start and will set you up for the future.

I loved your question, while it seems a simple one “investment options that offer both security and high returns”, what you’ve asked for is actually the holy grail of investing.

When investing, there is a trade-off between risk and reward – the higher the risk, the higher the potential reward, so effectively there is an inverse correlation between the two things you’ve asked for. During the last 20 years as an adviser and accountant, I’m yet to see an investment that can offer both these things reliably over the long term.

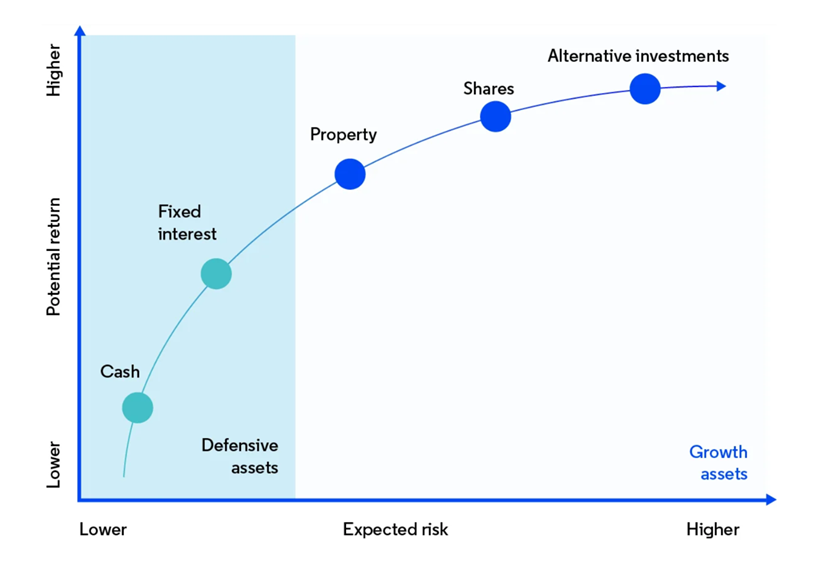

Depending on the asset class there are different levels of risk and reward with the chart below detailing the general performance over time.

Source: Moneysmart.gov.au

In my view, there are 3 good options for you:

-Apply the funds to your existing mortgage. Whilst not particularly exciting (and also not what you asked for!), this option will deliver you both security and a high return. The funds are secure as they have reduced a debt you currently have and have produced a high return of your mortgage rate (probably 6% or more). This return of approximately 6% is worth a return of approximately 9% pre-tax in any other asset class (assuming a 32.5% marginal rate). This option is a very attractive one.

-Purchase a low-cost diversified index fund. If you’re committed to investing the funds, then as detailed previously there would be a trade-off regarding the risk and return. You would need to understand your appetite for risk as this will dictate how you invest the money. The investment options would likely be a Balanced, Growth or High Growth fund – each with different levels of defensive and growth assets.

When investing in shares or index funds, it is important to have a medium to long term time horizon to ensure any volatility (i.e. a stock market correction) can be tolerated. The returns for each of the types of funds are also different with the Growth and High Growth funds offering higher returns but with more risk. Potential returns are between 6.5% to 8.1% depending on the fund and are pre-tax (meaning you would pay tax on this return).

-If you want to focus on the high returns and are willing to sacrifice some security, then investing in shares is an option. When investing in shares, you can do it directly, i.e. you choose the shares and buy them via an online broker, or you could invest in a low cost share fund and a manager will choose the shares on your behalf. US and Australian shares have historically produced very good returns over time (9% to 10% pre-tax) but do come with increased volatility. As an example, during the COVID pandemic, the ASX 200 lost more than 30% of its value in less than a month (however, most of that loss was recouped over the next 12 months).

So there you have it, 3 good options for you to consider. If you asked me what I’d do, then I’d go with paying off the mortgage. In this market, it’s a guaranteed return that is higher than most investments can produce over the long term and improves your ownership in your own home.

All the best Rajesh, please reach out if you have any follow up questions or if your mortgage rate is much higher than 6%!

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0