"With tax implications in mind, should I leave cash in an at-call account or put it in super and start being paid money from it?"

- Question from Michael in Williamtown, NSW

Top answer provided by:

Michal Lancemore

Hi Michael,

Thanks for sending in such a juicy question! There are several significant aspects to your question (and I have made a number of assumptions), which is why I would highly recommend you obtain personal specialised financial advice! Call me!

1. Ubank is offering a great at call interest rate of 5% pa at present. However, any interest earned on the cash will be taxed in your hand (I’m assuming it is in your name Michael as the lower income earner) at a marginal rate of 19% (payable on income earned between $45K and $18,200) which equates to approximately $4,465 tax.

2. As you have reached your preservation age and retired, you have met a condition of release meaning you can access your entire super balance.

3. From a tax perspective, by moving a big chuck of cash into super and converting to a pension means you will pay ZERO tax on the interest/earnings (in superannuation phase, the earnings are taxed at 15%).

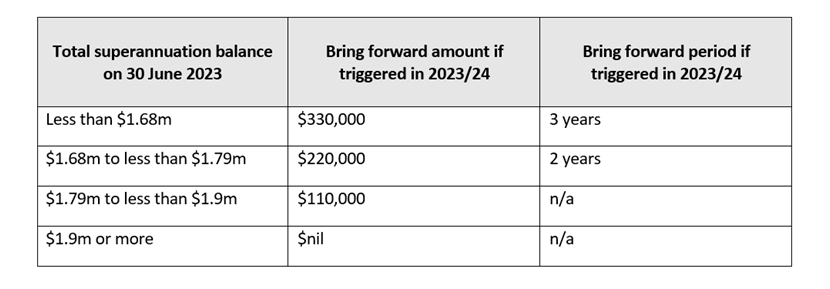

4. Depending upon your contributions history and superannuation balance* (I will assume you have <$1.68million), you can contribute up to $330K to your superannuation fund this financial year (triggering the bring forward rule).

5. Alternatively, given your wife intends to work for only another year or two, you and your wife can contribute approx. $230K each into your respective super funds. This will leave you with an available non-concessional cap of $100K each for the following 2 financial years. (Note: with the understanding that your wife is still unable to access any capital from her superannuation until such time as she meets a condition of release).

6. With tax implications in mind:

-Michael - assuming a 5% pa return, by moving $230K cash into your super fund and converting to pension, this instantly saves you 19% tax (or $2,185).

-Your wife - assuming a 5% pa return, by moving $230K cash into your wife’s super fund, you will save 4% tax (or $460).

Compared to simply retaining the cash in a high interest bearing account in your personal name, this super/pension strategy saves almost $2,000.

7. Moving to pension phase obligates you to draw a minimum age based pension payment each year. At age 60, this is 4% pa. If you do not require the income, you can elect to have the funds paid annually as one payment and contribute the funds back into superannuation as a non-concessional contribution (assuming you have not maximised the $330K cap).

8. Alternatively, should you need a tax deduction, you can elect to convert some of that non-concessional contribution to a concessional contribution and pay only 15% tax. This will depend on your taxable income for the year.

Superannuation provides the potential of significantly more diversification that simply cash. However, if you are concerned about how the markets will be affected by economic uncertainty, you can still retain the funds in a cash account within the super/pension environment – with significantly better tax outcomes.

On a side note: I would also encourage you to utilise superannuation when you sell the property as this can be a great way to reduce any associated CGT.

Michael, in a nutshell, moving your superannuation to pension phase is a taxation strategy, not an income strategy. As I mentioned, if you do not utilise the pension income you are drawing, it can be contributed back into superannuation.

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0