"I currently pay low amounts on my HELP debt through my compulsory repayments and with upcoming and ongoing CPI increases, the outstanding balance has barely been reduced. Should I make voluntary contributions?"

- Question from Callum in Melbourne, VIC

Top answer provided by:

Michal Lancemore

Hi Callum,

Thanks for your question – it’s one that’s on the minds of three million Aussies who have tertiary debt. I wish the answer was black and white!

Whilst HELP debt is interest free, it is indexed every 1 June in order to ensure its value is adjusted in accordance with the cost of living. It is of particular interest this year given the Australian Bureau of Statistics has just released the indexation rate of 7% – a long way from the average 2% over the past 10 years.

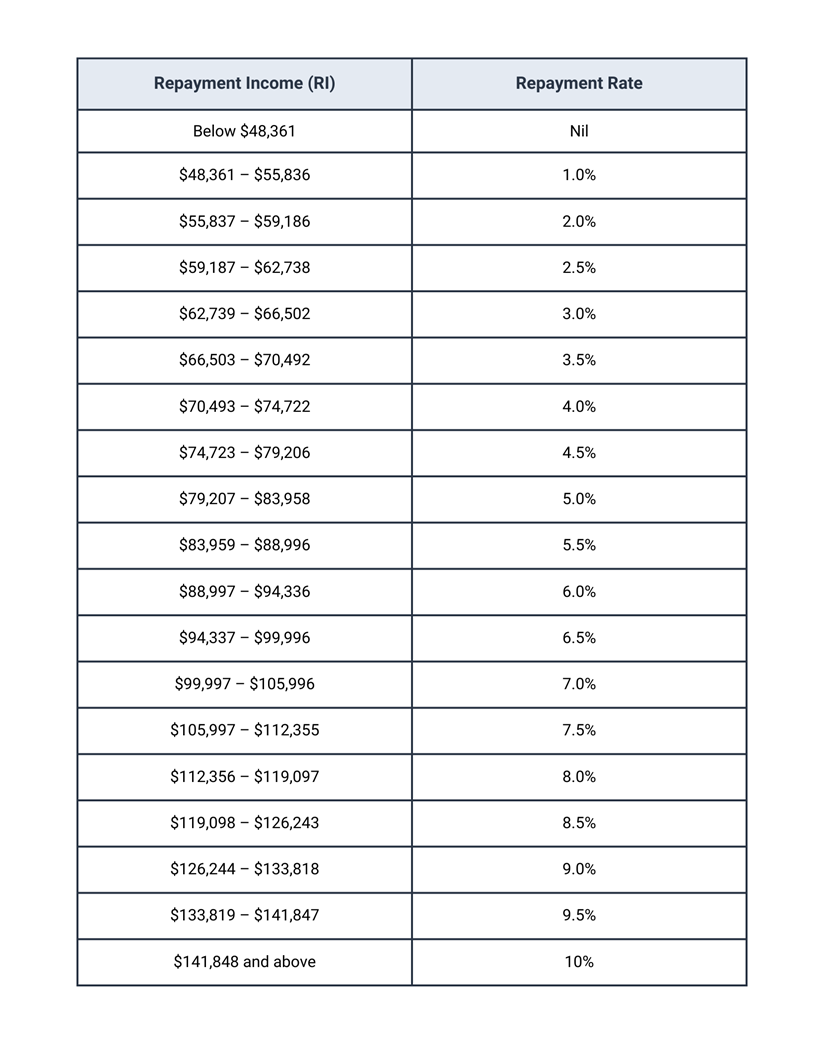

In previous years, the question of whether to make voluntary payments to reduce HELP debt was a non issue. However, given this year’s indexation is likely to add an additional $1,700 to the average debt of $25K, making only compulsory repayments based on your income may not even make a dent in the original balance.

2022-2023 repayment income thresholds and rates

BUT, does that automatically mean you should make voluntary repayments? As I said earlier, there’s really no ‘one-size-fits-all’ answer – it depends on your income, your expenses, your circumstances, and what’s most important to you. Consider the following question:

1. What is your inflation outlook?

If you believe the RBA will succeed at their job of easing inflation, then next year’s indexation rate will be much more palatable. The March quarter figures released by the ABS show that inflation has fallen from it’s peak of 7.8% - as an aside, this may see the RBA cease their interest rate hikes and potentially cut them later in the year.

2. Do you have any other debts?

If you have other debts, like credit cards or personal loans, these are likely to have much higher costs and should be reduced prior to paying down debt that attracts nil interest.

3. Do you have any other financial goals and objectives?

Generally individuals with these debts are younger and therefore arguably better off utilising surplus cashflow to support other goals – ideally investing in either property or the sharemarket. There is an opportunity cost is using any surplus income to pay off HELP versus investing in an asset class that has historically outperformed inflation.

4. Do you plan on applying for finance in the near future?

HELP/HECS debts can affect your borrowing capacity when looking at finance (as your cashflow is affected). If you have a reasonable deposit, it is worth speaking to a finance broker to determine how your capacity would change if you retained this lump sum VERSUS using some to reduce your tertiary debt.

For mine, ultimately, a debt is a debt and there is an obligation to repay it. Whether that be via the mandatory repayment rate or with added voluntary repayments, it is completely subjective and worth having a discussion with your financial planner to assess your personal position.

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments1

"Great breakdown of details re: HECS and things to consider before paying down."

Ron Pratap 11:20 on 04 May 23