“I am 61 and will soon be made redundant. If I pay off my mortgage, can I retire early or can I still work 3 days a week and receive pension from my superannuation?"

-Question from Tony in Yarraville, VIC

Top answer provided by:

Michal Lancemore

Greetings Tony!

Are congratulations in order?! Redundancy can be an opportunity in disguise, and it has its benefits in regard to accessing superannuation if you are made redundant after age 60.

I believe your question can be broken down into two parts:

1. Can I retire early after redundancy? and/or,

2. After redundancy, can I work part time and receive a superannuation pension?

To answer your first question – retiring early depends upon your personal circumstances. After you have paid out your mortgage, are you able to generate enough income from your remaining asset base to cover your income requirements?

I suspect what you are really asking is, “can I access a pension from my superannuation once made redundant, yet still work part time?”.

I spoke about this very topic on my YouTube channel back in June 2022. Check it out here.

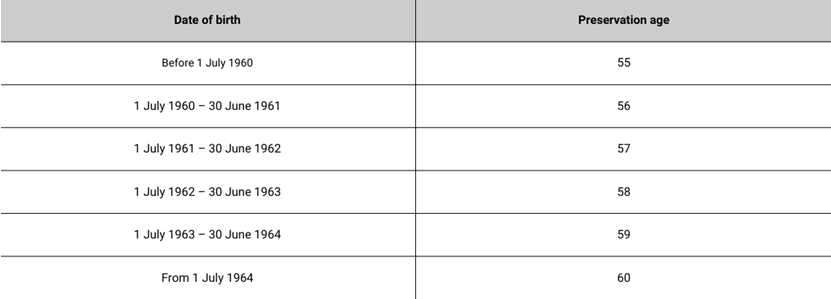

Preservation Age*

According to the super rules, to unlock the first level of access to your superannuation in any capacity you must reach your preservation age.

-At 61, you have achieved this, as all of us will have achieved our preservation age by age 60.

-Having met your preservation age, you can access your superannuation as an income stream only via a Transition to Retirement Pension.

-The income stream you can access must be at least 4% but no more than 10% of the account balance every year.

-You cannot access any of the account balance via lump sum withdrawals.

-The earnings on the assets within the Transition to Retirement pension are still taxed at 15% as per accumulation super.

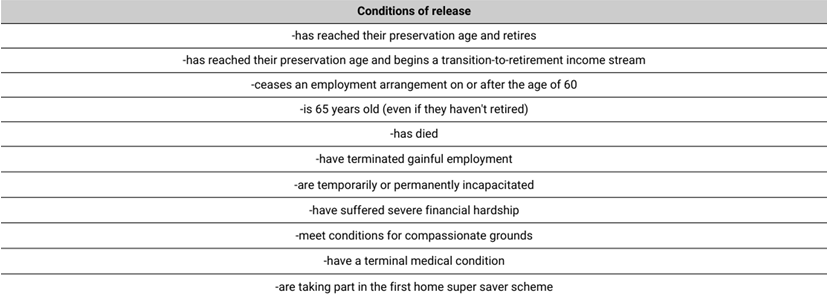

Condition of release*

To unlock the second level of access to your superannuation (i.e. lump sum access) you must also meet a condition of release. A common condition of release is retiring or reaching age 65. However, ceasing a gainful employment arrangement on or after age 60 is also a condition of release – and that’s you!

So, at 61 years of age, and having ceased an employment arrangement (by being made redundant), you are able to access your superannuation in two ways:

-Via an income stream (minimum but no maximum income stream requirements), and/or

-Via lump sum withdrawals

The benefits of meeting preservation age and a condition of release are that the amount converted from superannuation accumulation to pension phase is invested in a tax-free environment (up to the $1.7 million transfer balance cap):

-zero tax on the income payments you take out

-zero tax on earnings that the assets generate

-zero tax on any realised capital growth!

After being made redundant and accessing a pension from your superannuation, you can return to the workforce with another employer (not the employer who made you redundant!) at any time, in any capacity – either full time or part time.

It is important to note that any superannuation contributions that are accumulated once returning to the workforce are classified as preserved and are unable to be accessed until you meet another condition of release.

Tony, I highly recommend you speak to a qualified financial adviser to ensure your complete personal circumstances are considered prior to making any decisions.

*Preservation ages

*Conditions of release

While the Adviser Ratings Website facilitates the question and answer functionality, all such communications are between users and authorised financial advisers, of which Adviser Ratings has no affiliation. Adviser Ratings is not the advice provider and does not provide financial product advice and only provides information that is general in nature.

Article by:

Comments0