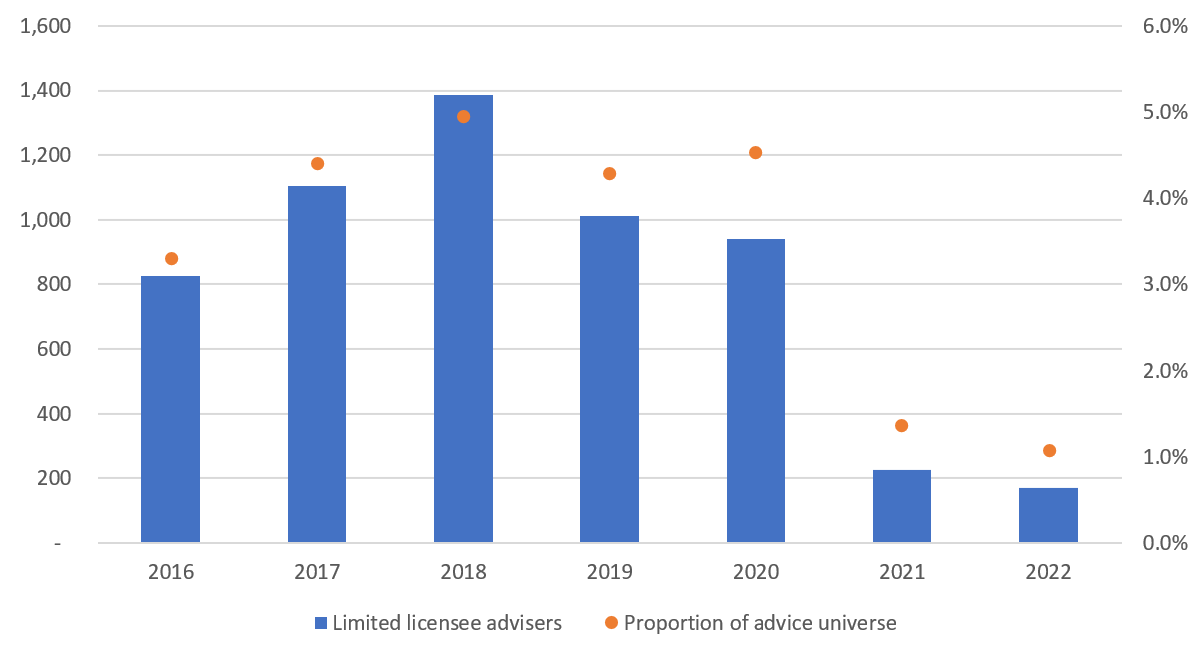

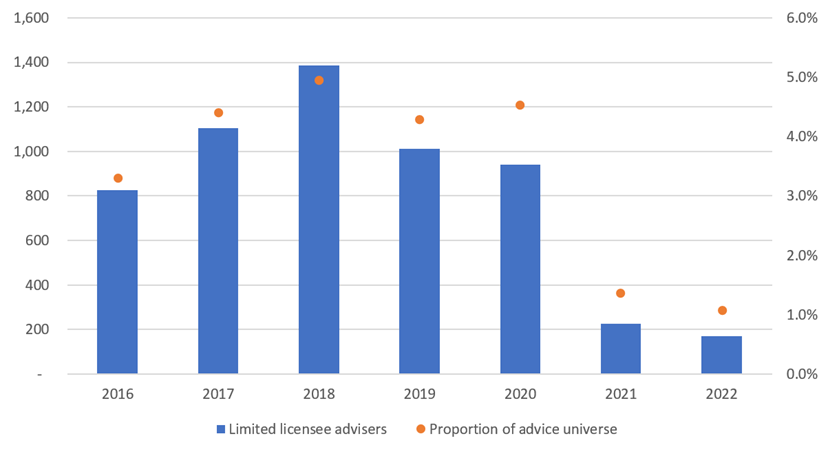

A few years ago, limited licensee advisers – primarily accountants – made up 5 per cent of the financial advice licensing landscape, Adviser Ratings analysis shows. In fact, there were more than 1000 operating under the once popular framework, which allows individuals or companies to provide narrowly defined financial product advice, often about self-managed super funds (SMSFs).

Today, the limited licensee model has all but collapsed, with bodies such as the Chartered Accountants of Australia and New Zealand calling it “unworkable”.

The vast majority of accountants have now handed back their limited licence, with administration and compliance-related costs, insurance and professional standards obligations among the reasons we’re told limited licensees are no longer viable.

The numbers speak for themselves. At the end of last year, there were fewer than 200 limited licensed advisers, accounting for just 1 per cent of the advice market, our data shows.

Figure 1 – The rapid decline of limited licensee advisers

Source: Adviser Ratings.

What does the Quality of Advice Review say?

In the Quality of Advice Review Final Report, reviewer Michelle Levy wrote that she was aware of the problems with limited licensees.

“Limited AFS licence-holders are still required to meet all of the relevant obligations that attach to a licensee, including complying with the general obligations of an AFS licensee, holding professional indemnity insurance, being a member of the AFCA and paying the ASIC levy and so, the benefits of a limited licence seem, well, limited,” she wrote.

Ms Levy noted that accounting and SMSF groups had suggested accountants should be able to provide some superannuation-related advice, such as whether to set up an SMSF, without a licence. Their reasoning included accountants’ existing education and trusted relationships with clients.

However, she said accountants should not receive an exemption from the licensing framework.

“Advice on superannuation products, including interests in SMSFs, is financial product advice. And it should be regulated as financial product advice. I do not see any reason for making an exception,” she wrote in the final report.

Ms Levy pointed out some of the issues related to limited licensees were outside the scope of her review, including professional indemnity insurance, education standards and the ASIC levy.

More broadly, she wrote, “The recommendations I make in this report will make it easier for all advice providers, including accountants who are authorised by an AFS licensee to provide this advice, to provide personal advice to their clients. It will also make it easier for them to provide limited or one-off advice.”

Accounting groups are expected to make further representations to Treasury as it consults on the Quality of Advice Review Final Report.

In the meantime, we expect limited licensee numbers to fall into double digits this year, as the segment evaporates further. It’s likely to follow the banks and become the second licensee type to completely disappear.

Article by:

Comments2

"The problem for Accountants and Insurance specialists, is they are being dragged along and forced to comply with a vast array of Regulatory and Education requirements that are NOT fit for purpose and have made it too hard to provide advice in their particular field of expertise. If we made the building Industry comply under similar requirements, then every trade would be forced to study and pass each individual trade qualification requirements due to the fact they all work in the same Industry. So every tradesman would no longer have the time or expertise to work in their own field, due to red tape / compliance anchors that would drive most out of Business and those that survived would dramatically increase their fees to offset the additional costs and risks imposed by the red tape / Education brigades. What we would end up with, is a shortfall in housing and those fortunate enough to be able to afford a home, or even renovate or maintain a home, would be paying substantially more and the vast majority of Australians would miss out. Sounds a bit like our Industry, though at least we could all take comfort that the vested interest groups in Education, Legal, Public service, Regulators etc, would still be able to live a wonderful life with total job security, while the economy and the rest of the population fall through the cracks and our Trillion dollar deficit continues to rise with meteoric speed. When the whole issue of churn raised it's head around Life / Disability advice, the Industry knew who the churners were and that problem, which was a tiny percentage of the Adviser population, could have been solved in ONE DAY at NIL COST to everyone. The solution was simple. Limit those Advisers to level commission and the problem goes away. What did we end up with? A NEVER ENDING series of investigations that refused to look at the real issues and instead, feathered their own nests by making a "mountain range" out of a mole hill, which coincidently made those entities millions of dollars, at the expense of ALL Australians. I and many others have for years been saying, that just like an Electrician or Plumber or Carpenter that specialises, trained and gained education in their own field, which enables them to work beside the other trade specialists, then the same should apply in the Financial services sector, where the upfront and ongoing Education requirements should be related and specific to the work and advice performed. Only then can we start to claw back and try to recover from what has been and continues to be a total fiasco and mismanagement of our Industry."

Jeremy Wright 16:03 on 29 Mar 23

"As an adviser of more than 4 decades with approved accreditation to give advice to SMSFs, I have recently started to not provide that kind of advice, because it is becoming too risky and so I tell people to find a specialist adviser for SMSFs that does nothing else, so the drop in numbers is not just from accountants. "

Roland Knight 15:25 on 29 Mar 23