Platinum Adviser and insurance specialist Jordan Ryan from Stanford Brown always hears the same objections for why people are yet to consider personal insurance, or why they haven’t reviewed their existing insurance portfolio. He sets the record straight here, busting some common myths people use to justify their decisions. Do any of these sound familiar to you???

Platinum Adviser and insurance specialist Jordan Ryan from Stanford Brown always hears the same objections for why people are yet to consider personal insurance, or why they haven’t reviewed their existing insurance portfolio. He sets the record straight here, busting some common myths people use to justify their decisions. Do any of these sound familiar to you???

Myth Number 1

“I don’t have kids or a mortgage, so I don’t need life insurance”

Many people confuse personal insurance as solely being protection in the event of death, and in the absence of financial dependents, may place little value on this type of cover. There are policies that do provide this type of protection, but there are others such as Total Permanent Disability (TPD); Trauma; and Income Protection insurance that you need to be considering much sooner in life, such as when you secure a full-time job.

You are your own greatest asset, and your future earnings over a lifetime of work can amass to millions of dollars. Yet 69% of Australians do not have insurance in place to protect their ability to work and earn an income should an injury or illness strike. This is extremely alarming considering actuarial analysis shows that six in ten Australians will be disabled for more than one month during their working life and one in four will be disabled for more than three months.

You insure your car, home, and even the beloved pet, so why are you overlooking the fact that this would all be worthless if the monthly pay cheque stopped coming through? The research also supports this, with a significant portion of Australians (38%) declaring that they could not survive greater than one month without their income before needing to sell personal assets, which jumps even further for those under age 35 (approximately 50%). Furthermore, looking at 2015 claim statistics from TAL, one of Australia’s largest life insurers, 77% of claims for males and 58% of claims for females before age 55 were due to illness or injury, not death.

I urge you to question your priorities, and consider how much your income means to you, as it could mean the difference between being forced to go back living with your parents vs buying your dream home; going on the yearly trip overseas; keeping the kids in school; purchasing that investment property; or even retiring on your own terms and not having to rely on Government assistance.

Myth Number 2

“I can’t afford the premiums”

Cashflow is a major factor that needs to be considered when building a tailored insurance portfolio. Ultimately we would all love to hold a few million dollars in cover, as a lot of us may actually need that much, but the end premium may see this as being unattainable for some. It is important however to distinguish between what you can afford and what you are willing to outlay on premiums. We can all reduce our unconscious spending on the little everyday things that do not add any significance to our lives if required, but as previously mentioned it comes down to prioritising what is most important to you.

Where a qualified adviser can add a lot of value is by working with you to ensure you get the mix right between directing your premiums toward the policies most relevant to you and your personal circumstances; obtaining a level of cover that you are comfortable with; whilst also offering advice on different ways of structuring your insurance to maximise overall tax efficiency. I think you may even be surprised at how inexpensive comprehensive cover can be, and if every cent of your income is precious to you, you can’t really afford not to have the cover in place.

Myth Number 3

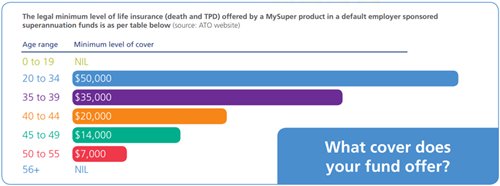

“I’m adequately protected by the cover in my super fund” Fig.1 Legal minimum level of default life insurance for Death and TPD offered by a MySuper product in a default employer sponsored superannuation fund.

Fig.1 Legal minimum level of default life insurance for Death and TPD offered by a MySuper product in a default employer sponsored superannuation fund.

Most superannuation funds automatically provide members with a basic level of default insurance when you join the fund (typically Death and TPD, and sometimes Income Protection but this is not a legal requirement of the fund).

However, the cover you receive is formula driven based on your age and salary, meaning it is not tailored to your specific needs. This often results in a noticeable gap between the level of cover that you hold and what you actually need. To provide some context, the legal minimum level of default life insurance for Death and TPD offered by a MySuper product in a default employer sponsored superannuation fund can be as low as $7,000 dependant on your age (See Fig. 1). I don’t need to point out the obvious that this level of cover is well and truly insufficient to even extinguish the average Australian mortgage, which is extremely concerning as I often hear “I’m covered through my super fund”.

The point must also be made that not all insurance contracts provide the same level of protection. Your default cover through superannuation for example is conveniently provided as you don’t need to fill out an application or disclose any details of your prior health history. The danger here however is that these contracts encompass weaker policy definitions, which can make claiming on the policy more difficult.

Can you tell me whether your TPD policy provides tailored protection in the event you cannot return back to work in your ‘own specific role’, or is it a broader assessment of your ability to do ‘any role’ for which you are suited by education, training or experience? What about your Income Protection? Have you financially endorsed your contract, or will you be required to provide financial evidence at time of claim, which may impact the potential payout due to having time away from work or a fall in your earnings? Additionally, will your Income Protection policy continue making payments through to age 70 if you are unable to return back to work, or will it only provide these benefits for a maximum of 2 – 5 years? The latter of each of these points are typical characteristics of the basic default insurance provided through your superannuation fund. If you struggle to have confidence in answering these questions for yourself, you may be at risk of being inadequately protected.

Myth Number 4

“I’m healthy, it won’t happen to me”

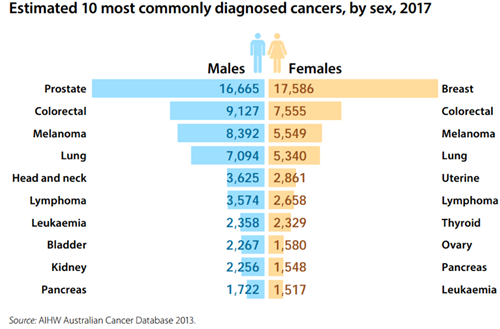

We all like to hope for the best, but you should also plan for the worst! An unexpected health event can occur at any time, no matter your age. Many people would struggle to say that they do not know someone within their network who hasn’t been impacted by an unforeseen illness, injury, or death. The most recent statistics released from the Australian Institute of Health and Welfare show that for cancer alone, men have a 1 in 3 chance of suffering from the illness, and women a 1 in 4 before the age of 75, with an average of 131 deaths every day. I can guarantee that a large number of these people also believed that they wouldn’t form part of the statistics. Obtaining insurance cover once a major illness or injury has occurred can prove very difficult, so the earlier you apply the greater chance you have at securing life-time cover with no premium loadings or policy exclusions. Fig. 2 Most commonly diagnosed cancers by sex (Est.)

Fig. 2 Most commonly diagnosed cancers by sex (Est.)

Reviewing your personal insurance position shouldn’t be something you continue to put off, as the consequences could be devastating. This is a complex area of financial planning that you need to get right, so I highly encourage you to seek the advice of a specialist adviser in this field to help ensure you do not become a victim of hindsight, which is summed up beautifully by the ancient Greek playwright Sophocles – “I have no desire to suffer twice, in reality and then in retrospect”.

Article by:

Comments1

"Timely article for me. They come in 3's. I thought I was covered by my super fund until I was directed by a mate to his adviser. What I had was not enough to cover the head of a pin. Look into it!"

Dave S 12:24 on 06 Dec 17